Selling in Florida

How Much Is My House Worth in Florida? (May 2026 Guide)

What your Florida home is really worth in 2026 - metro-by-metro values, why AVMs like the Zestimate are unreliable, and the accuracy ladder for getting a real number.

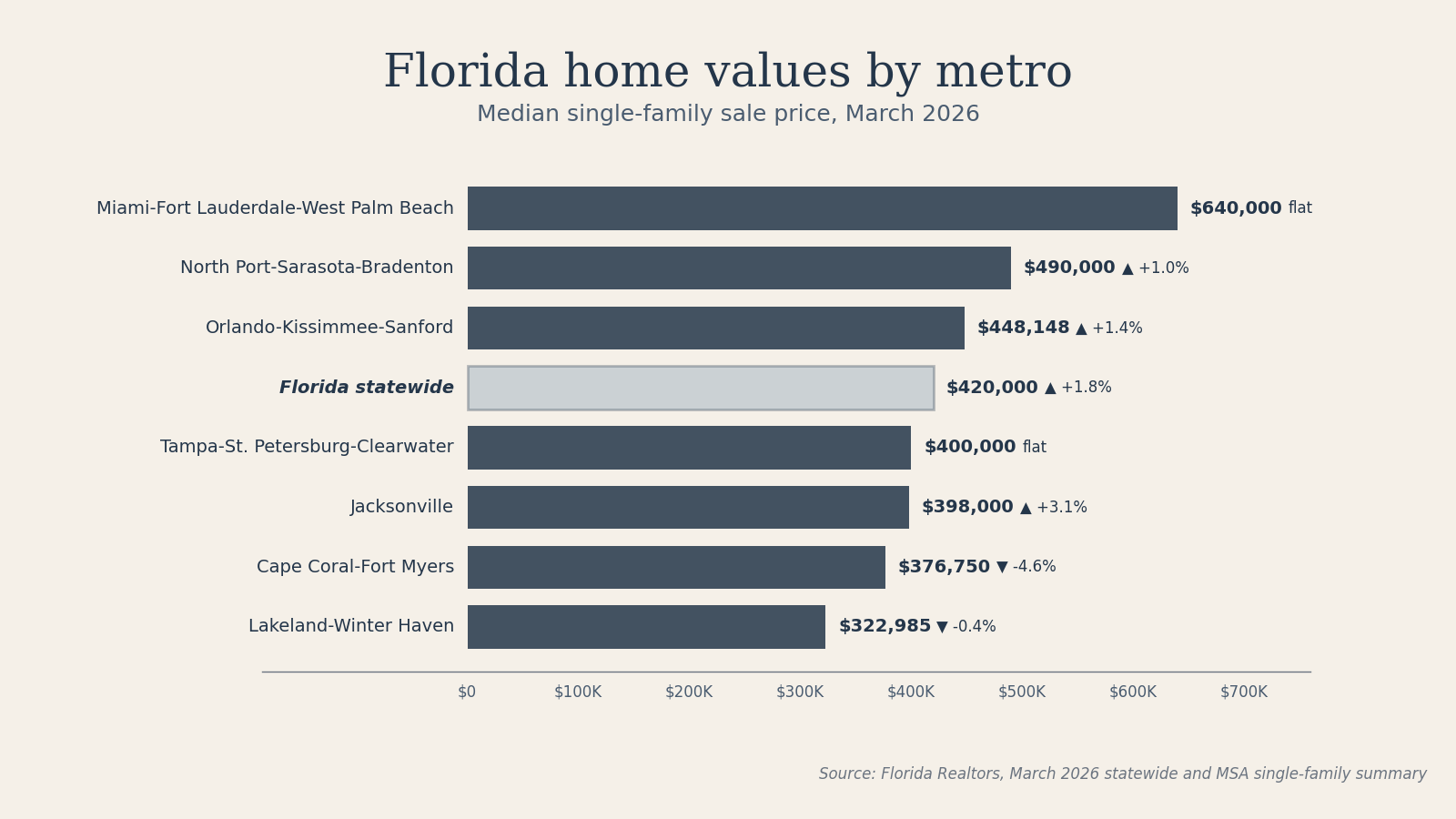

Florida home values in 2026 are not a single number. The same 1,800 square foot house can be worth $322,985 in Lakeland-Winter Haven, $400,000 in Tampa, or $640,000 in Miami. For a homeowner considering a sale, the first instinct is often to check an Automated Valuation Model (AVM) like the Zillow Zestimate or the Redfin Estimate. However, the accuracy of these tools depends entirely on whether your home is currently listed for sale. Data from the major portals reveals that the median error rate roughly quadruples for off-market homes, which is exactly what your home is until you put it on the market. This means the estimates most homeowners check first are often the ones they can trust the least. This guide walks through the current state of Florida home values by metro, explains why online estimates often miss the mark, and provides an accuracy ladder to help you find a real number for your property in 2026.

1. The State of Florida Home Values in 2026

The Florida real estate market in 2026 is defined by fragmentation. While the statewide median sale price for a single-family home in March 2026 sat at $420,000, representing a 1.8% increase year over year, the headline number does not tell the whole story. The market is effectively split between property types and geographic regions. There were 102,288 active listings in March, but the absorption of those listings varies dramatically based on whether you own a detached house or a condominium.

For single-family homes, the statewide supply stands at 4.8 months. This is widely considered a balanced market, where neither buyers nor sellers hold a significant advantage. However, the statewide condo-townhouse supply has reached 9.1 months, which is a much looser market that favors buyers. This means the type of property you own is just as important as where it is located. In May 2026, the typical Florida seller is seeing a market that is slower than the pandemic boom years, with a median of 51 days to get a contract and 91 days to reach a final sale.

2. How Florida Metro Markets Compare Right Now

To understand what your house is worth, you must look at the specific metro market where the property sits. Florida’s metros are currently grouped into three distinct buckets based on inventory levels and price movement.

Tight and Stable Markets

Tampa-St. Petersburg-Clearwater and Jacksonville remain the fastest moving metros. In Tampa, the median price is $400,000, which is flat year over year, but the supply is tighter than the state average at 3.7 months. Jacksonville has seen prices rise to $398,000, a 3.1% increase, also with a relatively tight 3.7 months of supply. These areas are characterized by steady demand and faster transaction times, with Jacksonville properties going to contract in a median of 40 days.

Balanced Markets

The bulk of the state, including Orlando, North Port-Sarasota-Bradenton, and Lakeland-Winter Haven, sits in the balanced bucket. Orlando’s median price is $448,148, up 1.4%, with a 5.09 months supply. Sarasota follows a similar path with a median of $490,000, up 1.0%, and 4.8 months of supply. Lakeland-Winter Haven remains one of the more affordable options at $322,985, though prices there have dipped slightly by 0.4%. In these markets, sellers must be more precise with their pricing to avoid sitting on the market, as evidenced by Orlando’s 77 days on market.

Softer Markets

Cape Coral-Fort Myers and the South Florida condo submarkets are seeing the most pressure. In Cape Coral-Fort Myers, the median single-family price has dropped 4.6% to $376,750, with supply elevated at 5.4 months. Miami-Fort Lauderdale-West Palm Beach remains the most expensive metro with a median price of $640,000, but inventory is growing, with a county-level supply range between 4.7 to 5.7 months. In these areas, buyers have more leverage to negotiate on pre-sale repairs in Florida and other concessions.

3. Why AVMs Like the Zestimate Are Unreliable for the Homes That Matter Most

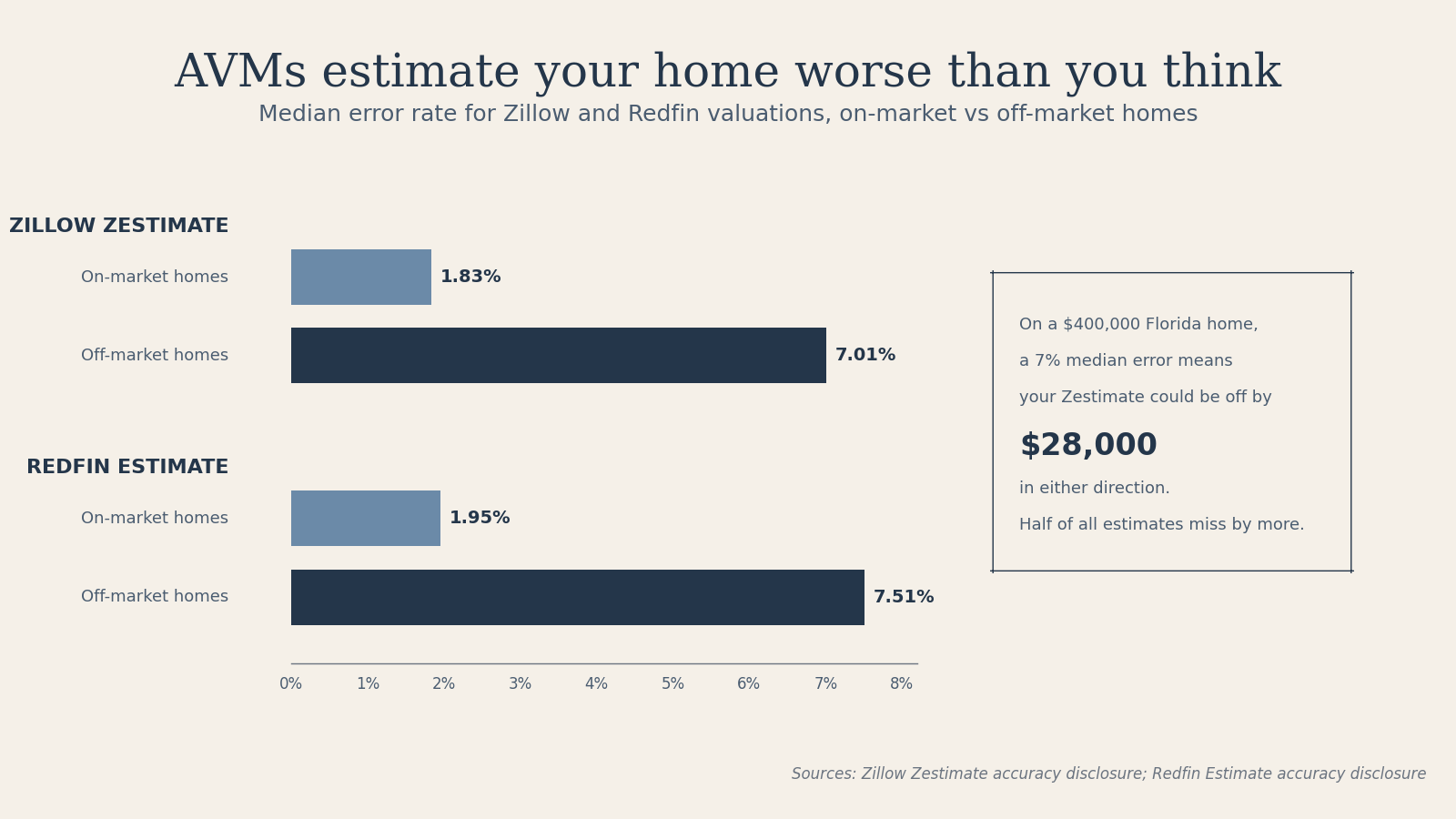

Most Florida homeowners start their valuation journey with an Automated Valuation Model (AVM) like Zillow’s Zestimate or the Redfin Estimate. These tools use public records, MLS data, and machine learning to estimate a value instantly. While they are useful for a quick curiosity check, their accuracy disclosures contain a major warning for prospective sellers.

According to Zillow’s own published data, the Zestimate has a national median error rate of 1.83% for on-market homes. However, for homes that are not currently listed for sale (off-market), that median error rate jumps to 7.01%. Redfin reports a similar trend, with a 1.95% median error for on-market homes and 7.51% for off-market homes.

This means that for a typical $400,000 Florida home that is not currently listed, the AVM is likely to be off by roughly $28,000 in either direction. It is also critical to remember that these figures are medians, meaning half of all estimates miss by even more than 7%. Both Zillow and Redfin explicitly state that these tools are not appraisals. They struggle with homes that have unique features, canal frontage, seawalls, or major repairs before selling. If your home is off-market, the AVM is essentially an educated guess based on neighborhood averages, not a reflection of your specific property’s condition or risks.

4. The Five Levels of Home Valuation in Florida (Accuracy Ladder)

Because AVMs have such high error rates for off-market homes, professional valuation relies on an accuracy ladder. As you move up the ladder, the cost and time increase, but so does the precision and the legal defensibility of the number.

-

Level 1: Free AVM (Zillow, Redfin, Realtor.com)

- Cost: Free

- Time: Instant

- Best for: Casual curiosity or a very rough starting range

- Failure mode: Misses property-specific condition, roof age, and building-level condo issues

-

Level 2: DIY Comp Analysis

- Cost: Free

- Time: 1 to 2 hours

- Best for: Sanity-checking an AVM by looking at what neighbors actually sold for

- Failure mode: Homeowners often pick the highest sales rather than the most comparable ones

-

Level 3: Agent CMA (Comparative Market Analysis)

- Cost: Usually free as part of a listing presentation

- Time: 1 to 3 days

- Best for: Setting a listing price or understanding local buyer behavior

- Failure mode: Can be influenced by an agent’s desire to win a listing; not a formal legal document

-

Level 4: Desktop or Drive-By Appraisal

- Cost: $200 to $400

- Time: 3 to 5 days

- Best for: Lenders who need a formal number but do not require a full interior inspection

- Failure mode: Limited scope means it can still miss interior condition issues

-

Level 5: Full USPAP Appraisal

- Cost: $500 to $800 or more

- Time: 1 to 2 weeks

- Best for: Lending, estates, divorce, tax challenges, and legal disputes

- Strengths: This is a formal opinion of value governed by the Uniform Standards of Professional Appraisal Practice (USPAP), the most defensible number available

5. The Florida-Specific Drivers That Move Your Home’s Value

In 2026, Florida home values are being moved by factors that are unique to the Sunshine State. Understanding these drivers is essential for a realistic valuation.

Mortgage Rates and Monthly Payments

The 30-year fixed mortgage rate stood between 6.18% to 6.2% in March 2026. While this is lower than the peaks of 2024, Florida buyers are particularly sensitive to these rates. Because Florida property taxes and insurance premiums are often higher than the national average, the monthly payment on a Florida home is more sensitive to rate swings than a home in a lower-cost state. This payment sensitivity directly caps how much a buyer can offer for your property.

Insurance and Risk Rating 2.0

FEMA’s Risk Rating 2.0 has changed how flood insurance is priced. Instead of broad zones, insurance is now priced based on property-specific variables like distance to water, flood frequency, elevation, and rebuilding cost. This means two homes on the same street can have radically different insurance bills. A high insurance quote can effectively lower your home’s value because it reduces the amount of mortgage a buyer can qualify for.

The Condo Inventory Surge

The statewide condo-townhouse supply is 9.1 months, compared to 4.8 months for single-family homes. This inventory glut in the condo market is driven by rising association fees and new requirements for reserve funding and milestone inspections. If you own a condo, your value is no longer just about your unit’s granite countertops; it is about the building’s balance sheet, its insurance renewals, and its structural integrity.

Save Our Homes and Tax Assessments

Many longtime Florida homeowners are confused by the gap between their tax-assessed value and their market value. Under the Save Our Homes (SOH) amendment, the annual increase in assessed value for homestead property is capped at the lower of 3% or the prior year’s CPI change. Over 10 or 20 years, this cap can keep your assessed value much lower than what the house would actually sell for. However, Florida law requires the property to be reassessed to its full just value the January 1 after a change of ownership. This is why a buyer’s future tax bill will often be much higher than your current one, a factor that savvy buyers will negotiate into the price.

6. What to Gather Before Any Florida Home Valuation

Whether you are talking to an appraiser or a local buyer, having a complete documentation package will ensure your valuation is based on facts rather than assumptions. You should gather the following items:

- County Property Record: Print your property card showing the parcel ID, legal description, heated square footage, year built, and current homestead status.

- Tax Documentation: Your most recent tax bill and any documents related to Save Our Homes portability.

- Upgrade History: A list of major upgrades with invoices and permit history. Focus on the roof, HVAC, windows, kitchen, baths, seawall, and pool.

- Insurance and Risk Info: Your current insurance declaration page, any wind-mitigation or 4-point inspection reports, and an elevation certificate if your home is in a flood zone.

- Condo Specifics: For units in an HOA or condo, gather the current budget, reserve study, board minutes, and any notices of special assessments.

Having these documents ready allows a professional to adjust for the specific things that add value to your home. In Florida, the age of your roof and the elevation of your finished floor can swing a valuation by tens of thousands of dollars.

7. The Fastest Path to a Real Number: A Direct Cash Offer

The accuracy ladder exists because traditional home valuation is difficult. Free AVMs are often inaccurate for off-market homes, CMAs are just opinions, and full appraisals are expensive and slow. For homeowners who need to know exactly what they will net from a sale without the stress of listing, there is a faster path.

A direct cash offer from Merit Closings Home Buyers is a real number from a real buyer. Merit reviews the property, analyzes the same comparable sales an appraiser would, and provides a market-value cash offer based on current market conditions. This eliminates the need for an appraisal contingency, a financing contingency, or an insurance contingency.

Merit Closings has 73 homes purchased in Florida with over $23 million in offers extended to homeowners. Merit closes in an average of 13 days and the seller pays $0 closing costs because Merit pays all of them. This is particularly helpful for homeowners who want to skip the uncertainty of an FSBO sale or the expense of Florida home seller closing costs.

For those in the Tampa Bay region, you can learn more about Merit’s Tampa-area home buying service and see how Merit evaluates properties in Hillsborough County. For all other Florida homeowners, you can see how Merit’s process works or get started today to sell your Florida house fast. Please note that we do not act as a realtor when we purchase properties directly from homeowners.

Frequently Asked Questions

How do I find out what my Florida house is worth right now?

Start with two AVMs (Zillow Zestimate and Redfin Estimate), then pull three to six recent comparable sales in your immediate area. The AVM gives you a rough starting range; the comps give you a directional check. If you need a defensible number for lending, divorce, estate, or a tax challenge, get a full appraisal from a licensed Florida appraiser.

Can I trust the Zestimate or Redfin Estimate for my Florida home?

Both companies state their tools are not appraisals. Zillow’s Zestimate has a 1.83% median error for on-market homes but 7.01% for off-market homes; Redfin Estimate is similar at 1.95% and 7.51%. On a $400,000 Florida home, that 7% off-market median error is a $28,000 swing in either direction, and half of all estimates miss by more than that.

Why is my tax-assessed value so different from what my house could sell for?

Florida’s Save Our Homes cap limits the annual increase in assessed value on homestead property to 3% or the prior year’s CPI change, whichever is lower. Over many years, that cap can push your assessed value far below market value. Florida law also reassesses the property to just value when it changes ownership, which is why a recent buyer’s tax bill can jump sharply.

How does flood zone affect my home's value in Florida?

Flood zone affects insurance premiums, which directly affect what a buyer can afford to pay for the property. FEMA’s Risk Rating 2.0 prices flood insurance based on property-specific variables like distance to water, elevation, and rebuilding cost, so two homes on the same street can carry very different insurance costs. A high-risk flood zone or a poor elevation profile can shrink your buyer pool meaningfully. For broader seller questions, review the Merit Closings FAQ page.

What's the fastest way to get a real value for my Florida home?

A direct cash offer from a buyer like Merit Closings Home Buyers is a real number from a real buyer, typically delivered within a few days of property review. Merit purchases properties in any condition with no inspections, repairs, or financing contingencies. Sellers see exactly what they would net, with $0 closing costs, in an average closing time of 13 days.

Sources

- Florida Realtors, March 2026 Single-Family and Condo Market Reports, https://www.floridarealtors.org/news-media/reports/florida-market-reports

- Zillow, Zestimate Accuracy Disclosures, https://www.zillow.com/z/zestimate/

- Redfin, Redfin Estimate Accuracy Disclosures, https://www.redfin.com/redfin-estimate

- Florida Department of Revenue, Save Our Homes and Assessment Limitation FAQ, https://floridarevenue.com/property/Pages/LocalOfficials.aspx

- FEMA, Risk Rating 2.0: Equity in Action, https://www.fema.gov/flood-insurance/risk-rating

- The Appraisal Foundation, USPAP Standards, https://www.appraisalfoundation.org/

- Orlando Regional REALTORS Association, March 2026 Market Report, https://www.orlandorealtors.org/marketreports

- Northeast Florida Association of Realtors (NEFAR), March 2026 Market Statistics, https://www.nefar.com/market-stats/

- Fannie Mae, Appraisal Guidance and Sales Comparison Approach, https://selling-guide.fanniemae.com/

- National Association of Realtors, Existing Home Sales Reports March 2026, https://www.nar.realtor/research-and-statistics/housing-statistics/existing-home-sales