Selling in Florida

What Repairs Do I Need to Make Before Selling My Florida House? (2026 Guide)

What Florida sellers must fix before listing - the insurance and appraisal gates that can block financed buyers, plus what actually pays back at sale.

Selling a home in Florida is different than it was even five years ago. For a homeowner looking to sell a property today, especially one that might be older or in need of some work, the question is not just about what looks good to a buyer. Instead, Florida sellers now face two overlapping gates that determine whether a sale can actually close. These are the insurance underwriting gate and the mortgage appraisal gate. In many cases, a house can be cosmetically perfect but still lose every financed buyer if the roof is too old for a new insurance policy or if a specific type of electrical panel is found during an inspection. This guide walks through which repairs are mandatory for a traditional sale, which ones are a waste of money, and how the Florida insurance market in 2026 has changed the math for every homeowner.

1. The Two Gates Every Florida Home Must Pass to Close

When you list a home on the open market, your most likely buyer is someone using a mortgage. Whether they use a Conventional loan or an FHA loan, their lender will not release the funds until two specific hurdles are cleared. If a property fails either of these hurdles, the deal usually dies, or the seller is forced to make expensive, last-minute repairs to save the transaction.

The first gate is insurance underwriting. In Florida, almost no lender will issue a mortgage unless the buyer can prove they have a bindable homeowners insurance policy. Because the Florida insurance market has been under extreme pressure, insurance companies have become the de facto building inspectors of the state. They use a tool called a 4-point inspection to look at the roof, electrical, plumbing, and HVAC systems. If any of these systems are too old or have specific defects, the insurer will refuse to cover the home. No insurance means no mortgage, and no mortgage means no sale.

The second gate is the mortgage appraisal. While an inspector looks for everything that might be wrong, an appraiser looks for things that affect the safety, soundness, and structural integrity of the home. Fannie Mae and the FHA have strict condition standards. If an appraiser sees a leaking roof, rotting wood, or a broken window, they will mark the appraisal “subject to” repairs. This means the loan is not approved until the seller fixes those specific items and an inspector verifies the work. Understanding these gates is the key to knowing where to spend your repair budget and where to save it.

2. Who Can Buy Your Florida Home, and What Each Buyer Type Requires

The type of buyer you attract determines the repair standard you must meet. As you move from cash buyers to government-backed loans, the property condition requirements become increasingly strict.

Cash buyers represent the most flexible pool. Because there is no lender involved, there are no mandatory repair standards. A cash buyer can choose to buy a house with a leaking roof, a failed HVAC system, or even structural foundation issues. This is why cash sales are common for inherited homes or properties that have been vacant for years.

Conventional buyers, who typically use Fannie Mae or Freddie Mac financing, fall in the middle. Their appraisers are required to flag any physical deficiencies that affect the safety or structural integrity of the building. This includes items like active roof leaks, unresolved structural movement, or hazardous electrical systems. The lender must document that these issues have been corrected before the loan can be delivered.

FHA buyers face the highest bar. The FHA appraisal protocol requires the appraiser to look for anything that affects the livability and soundness of the property. This often includes minor items that a Conventional appraiser might overlook, such as peeling lead-based paint in older homes or the lack of a proper handrail on a staircase. If you are selling an older home that has been neglected, FHA buyers may be the hardest to satisfy without a significant pre-listing repair budget. Merit Closings Home Buyers offers an alternative to these hurdles by providing a market-value cash offer that removes the financing and appraisal gates entirely.

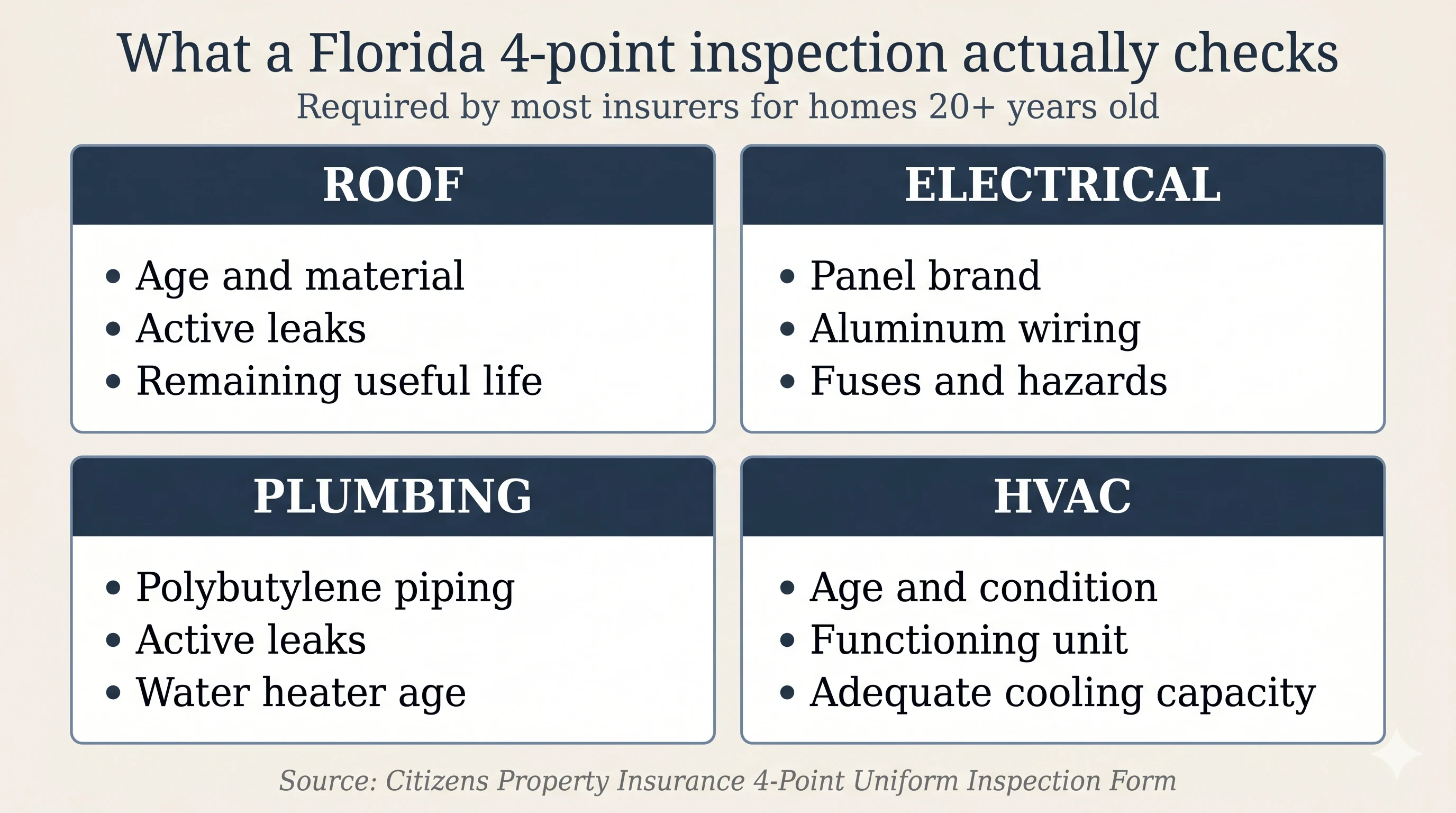

3. What a Florida 4-Point Inspection Actually Checks

For any Florida home more than 20 years old, a 4-point inspection is almost universally required by insurers before they will bind a new policy. This inspection is a focused review of the four major systems that represent the highest risk for insurance claims. It usually costs between $100 to $300 and can be the single most important document in a Florida real estate transaction.

The roof is the first and most critical component. Insurance companies in Florida have moved toward very strict roof-age underwriting. According to guidelines from Citizens Property Insurance, which many private carriers follow, shingle or “soft” roofs older than 25 years generally require documentation of at least five years of remaining useful life or a full replacement. For “hard” roofs like tile, metal, slate, or concrete, that threshold is 50 years. If a roof has active leaks or visible damage, it will fail the 4-point inspection regardless of its age.

The electrical section of the 4-point inspection screens for fire hazards. Inspectors look for branch-circuit aluminum wiring, which is common in homes built in the late 1960s and early 1970s, as well as outdated fuse boxes. Perhaps more importantly, they look for specific brands of electrical panels that are known to fail. If your home has a panel made by Federal Pacific, Zinsco, Sylvania, Challenger, or Pushmatic, most Florida insurers will require it to be replaced before they provide coverage.

The plumbing and HVAC sections check for active leaks and functional utility. Inspectors look at the age of the water heater and the material of the pipes. Polybutylene plumbing is a major red flag that often triggers a requirement for a full repipe. Finally, the HVAC system must be in good working order and capable of cooling and dehumidifying the home, which is essential for preventing mold growth in the Florida climate.

4. Florida-Specific Issues That Block Closings

Beyond the general inspection items found in every state, Florida has a unique set of “closing blockers” that can stop a sale in its tracks. These issues are often tied to the state’s building history, its environment, and its strict insurance regulations.

Polybutylene plumbing is a legacy issue from homes built between 1978 to mid-1995. These grey plastic pipes were widely used in Florida but are known to become brittle and burst over time. Many insurers will not cover a home with this plumbing, and the cost to repipe a home typically ranges from $1,500 to $15,000, with an average cost of around $7,500.

Electrical hazards are another major hurdle. Replacing an obsolete or hazardous electrical panel typically costs between $518 to $2,188, though complex jobs can exceed $4,500. If the home still has aluminum branch-circuit wiring, the cost to remediate the connections can be even higher. Because insurance companies often refuse to bind coverage until these items are fixed, they are rarely optional for a seller who wants to attract a financed buyer.

Moisture and mold are constant battles in Florida. The Centers for Disease Control and Prevention (CDC) notes that mold grows wherever moisture persists, including leaks in roofs, windows, or pipes. Mold remediation can cost between $1,223 to $3,755, but that does not include the cost of fixing the leak or rebuilding the damaged walls. Closely related are termites and other wood-destroying organisms (WDO). In Florida, drywood termite tenting or fumigation typically costs $2,000 to $5,000. If an appraiser or inspector finds active infestation or unrepaired structural damage from termites, it must be corrected before a loan can close.

Finally, sinkhole history and foundation issues are significant in certain Florida markets. Under Florida Statute 627.7073, a seller must disclose if a sinkhole claim was paid by an insurer. Foundation repairs in Florida are tiered based on severity: minor repairs might cost $3,000 to $7,000, while major stabilization using helical piers can range from $10,000 to $25,000 or more.

5. What Repairs Actually Pay Back at Sale

One of the hardest lessons for Florida sellers is that major system repairs rarely pay back their full cost at the time of sale. If you spend $20,000 on a new roof just to make the house sellable, you are not necessarily increasing the value of the home by $20,000. Instead, you are often just making the home eligible for a mortgage.

Data from the 2024 Cost vs. Value report for the Orlando metro area highlights this reality. Only a few projects actually recoup more than they cost:

- Steel entry door replacement: 230.6% recouped

- Garage door replacement: 191.8% recouped

Most other major projects result in a net loss of equity for the seller:

- Vinyl window replacement: 74.2% recouped

- Midrange bath remodel: 63.8% recouped

- HVAC electrification: 57.4% recouped

- Metal roof replacement: 47.3% recouped

The math here is sobering. If you spend $20,000 on a new metal roof, the data suggests you may only see about $9,460 of that reflected in a higher sale price. This results in a net loss of $10,540 compared to selling the home without making the repair.

The strategy for most sellers should be to focus on low-cost curb appeal and mandatory gate repairs. Spending money on a high-end kitchen remodel or a luxury master bath is usually a mistake for a seller in a distressed situation. These discretionary upgrades rarely recover their full cost. It is much more effective to focus on fresh exterior paint, basic landscaping, and fixing the major systems that would otherwise prevent a buyer from getting insurance or a mortgage. When you are calculating your potential proceeds, it is also important to factor in Florida home seller closing costs and how they interact with your total repair budget. You can get a better sense of what your Florida house is worth by looking at recent sales of homes in similar condition.

6. The Florida Insurance Crunch in 2026 and Why It Matters Now

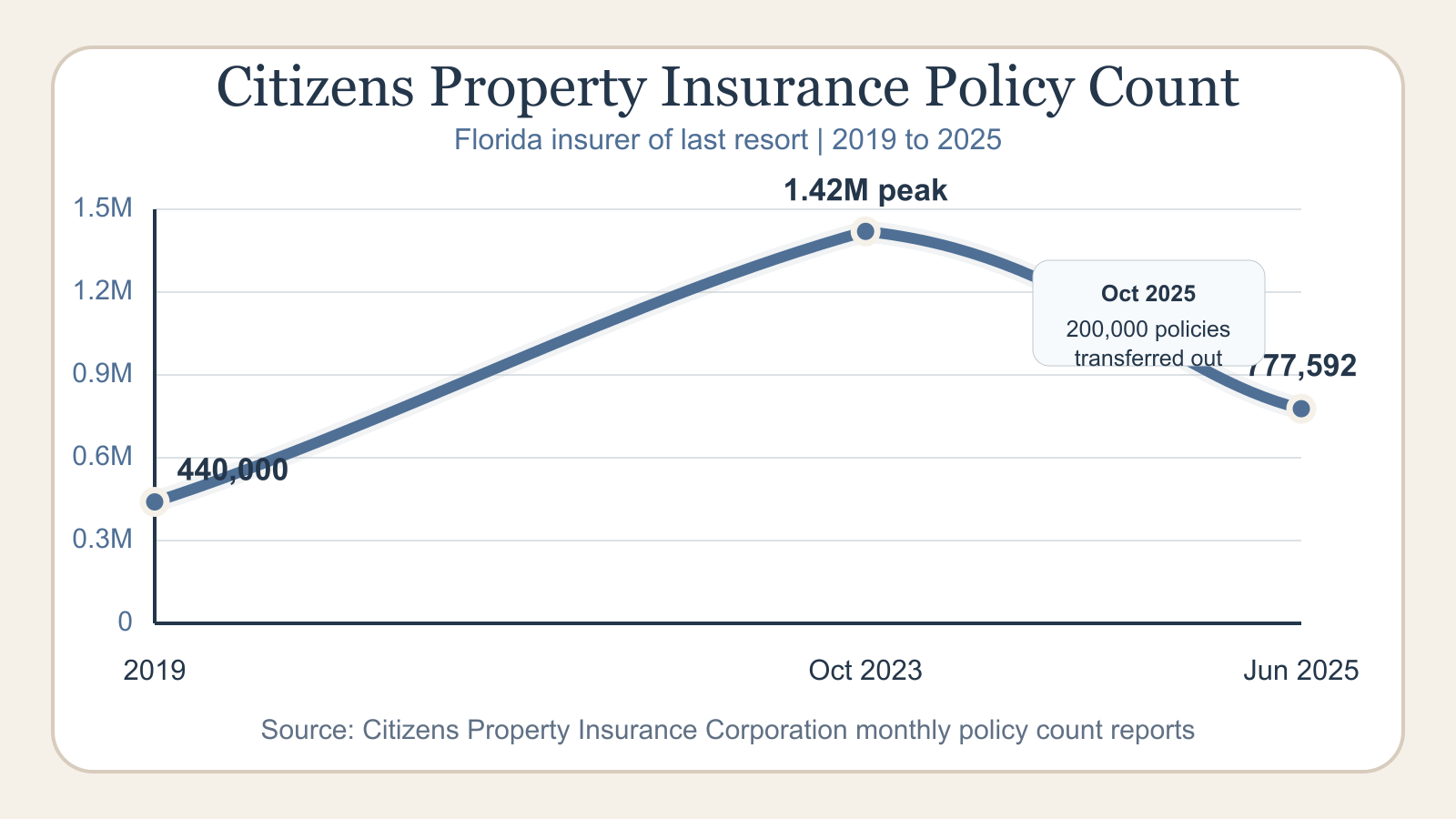

To understand why repairs are so critical in 2026, you have to look at the state of the Florida insurance market. For several years, Florida has been the most difficult insurance market in the United States. This environment has forced insurance companies to be extremely picky about which homes they will cover, turning them into the ultimate gatekeepers of real estate transactions.

The story is best told through the policy count of Citizens Property Insurance Corporation, the state-backed insurer of last resort. In 2019, Citizens had a baseline of approximately 440,000 policies. As private insurers fled the state or went bankrupt, that number exploded, peaking in October 2023 at 1.42 million policies. By June 2025, that count had fallen to approximately 777,592 as the state began an aggressive depopulation program, moving policies back to private carriers. In a single week in October 2025 alone, Citizens transferred approximately 200,000 policies to private companies.

The instability of the market was driven by a massive disparity in litigation. The Florida Office of Insurance Regulation reported that in 2022, Florida accounted for 70.5% of all homeowners insurance lawsuits in the country, despite having only 15% of the claims. This led to a crisis where seven major Florida insurers were ordered into liquidation between February 2022 and February 2023, including companies like United Property and Casualty, FedNat, and St. Johns.

For a homeowner today, this means that insurance companies are looking for any reason to say no. They are using drone photography and strict 4-point inspections to find old roofs, overhanging trees, and outdated electrical panels. If your home has these issues, it is not just a matter of price, it is a matter of whether the home is even insurable. This insurance crunch is why selling without a realtor or a FSBO sale often fails: owners underestimate how difficult it is for a retail buyer to secure coverage for a property with deferred maintenance.

7. The “As-Is” Trap and the Direct Cash Sale Alternative

Many Florida sellers believe they can avoid the repair conversation by simply listing their home as-is. This is often a misconception. While the Florida Realtors / Florida Bar AS IS Residential Contract releases the seller from the legal obligation to make repairs, it does not solve the problem of the two gates.

First, an as-is label does not waive your legal duty to disclose. Under the Florida Supreme Court case of Johnson v. Davis, a seller must disclose all known facts that materially affect the value of the property and are not readily observable by the buyer. The standard Florida Realtors disclosure form covers everything from polybutylene pipes to sinkhole history. Furthermore, as of October 1, 2024, Florida sellers must provide a residential flood disclosure stating whether they have filed a flood insurance claim or received federal flood assistance.

Second, an as-is contract does not stop the buyer from inspecting. The standard contract gives the buyer a strong cancellation right during the inspection period, which they can exercise in their sole discretion. If their 4-point inspection comes back with a failing grade, or their appraiser flags a safety issue, the buyer will still ask for a price credit or a repair. If you refuse, they can simply cancel and move on. You are then left with a house that has a known, disclosed defect that will likely stop the next financed buyer as well.

This is where a direct cash sale provides a massive advantage. Selling directly to Merit Closings Home Buyers eliminates both gates entirely. As a cash buyer, Merit does not require a bindable insurance policy to close. There is no mortgage lender, so there is no appraisal gate and no list of mandatory repairs.

Merit Closings has 73 homes purchased and has made over $23 million in offers to Florida homeowners. Merit provides a market-value cash offer and closes in an average of 13 days. The seller pays $0 closing costs because Merit pays all of them. To be clear: we do not act as a realtor when we purchase properties directly from homeowners.

If you are dealing with an inherited home, a divorce, or a property that simply needs too much work for a traditional buyer, you can avoid the cost and stress of pre-listing repairs entirely. You can learn more about how Merit’s process works or get started today to sell your Florida house fast.

Frequently Asked Questions

Do I have to make repairs before selling my Florida house?

Florida law does not require sellers to make repairs before listing. However, the Florida Realtors residential disclosure form requires you to disclose known material defects, and most financed buyers will flag certain conditions during the inspection period or insurance binding. You can list as-is, but you cannot avoid disclosure or buyer due diligence by labeling the contract that way.

What is a Florida 4-point inspection, and do I need one?

A 4-point inspection is a focused review of four systems: roof, electrical, plumbing, and HVAC. Most Florida insurers require it for homes more than 20 years old before they will bind a policy. Sellers do not order 4-point inspections themselves, but the buyer’s insurer will, and the result determines whether your buyer can get coverage to close.

Can I sell my Florida house as-is without disclosing problems?

No. The Florida Realtors / Florida Bar AS IS Residential Contract releases the seller from the obligation to repair, but it does not waive the seller’s duty to disclose material facts under Johnson v. Davis. Sellers must still disclose known defects, and buyers retain the right to inspect and to cancel during the inspection period.

My Florida roof is over 25 years old. Will I have to replace it before I can sell?

Not necessarily, but it depends on your buyer’s financing and insurance situation. Citizens Property Insurance and most private carriers require shingle roofs over 25 years to have documented 5+ years of remaining useful life or be replaced before binding. If your buyer cannot bind insurance, they cannot close on a financed offer. Cash buyers do not have this constraint. For broader seller questions, review the Merit Closings FAQ page.

How does selling to a cash buyer change the repair conversation?

A direct cash sale removes the appraisal gate (no lender condition standards) and the insurance gate (no insurer underwriting). Merit Closings Home Buyers, for example, purchases properties in any condition without inspections, repairs, or financing contingencies. Sellers avoid the cost, time, and uncertainty of pre-listing repairs entirely. Merit pays all closing costs and closes in an average of 13 days.

Sources

- Florida Realtors / Florida Bar AS IS Residential Contract for Sale and Purchase, https://www.floridarealtors.org/

- Florida Realtors Seller’s Property Disclosure - Residential, https://www.floridarealtors.org/

- Citizens Property Insurance Corporation, 4-Point Inspection Underwriting Guidelines, https://www.citizensfla.com/

- Citizens Property Insurance Corporation, Monthly Policy Count Reports, https://www.citizensfla.com/

- Fannie Mae Selling Guide, Property Eligibility and Appraisal Requirements, https://selling-guide.fanniemae.com/

- FHA Single Family Housing Policy Handbook 4000.1, Appraisal Protocol, https://www.hud.gov/

- Florida Office of Insurance Regulation, Property Insurance Market Reports, https://www.floir.com/

- Florida Insurance Guaranty Association (FIGA), Insolvency Records, https://figafacts.com/

- Florida Statute 627.7073 (Sinkhole Insurance Claims Disclosure), http://www.leg.state.fl.us/

- Florida Statute 689.301 (Flood Disclosure - effective Oct 1, 2024), http://www.leg.state.fl.us/

- Johnson v. Davis, 480 So. 2d 625 (Fla. 1985), https://scholar.google.com/

- 2024 Cost vs. Value Report, Orlando Metro Edition, https://www.remodeling.hw.net/cost-vs-value/2024/

- Centers for Disease Control and Prevention, Mold and Health, https://www.cdc.gov/mold/

- InterNACHI Polybutylene Plumbing Inspection Guidelines, https://www.nachi.org/pb.htm

- #repairs

- #selling

- #Florida

- #cash buyer